Dollar-Cost Averaging a Swing Account: A Practical Guide to Passing Prop Firm Challenges

Every method in this guide runs on an FTMO swing account (see how the swing account works here), and that starting point is not arbitrary. A swing account allows positions to be held overnight, across weekends, and through news, which is a requirement for the strategies that actually reward a retail trader. Factor models such as momentum, value, quality, and low-volatility are medium-term instruments; the statistical relationships they exploit take weeks or months to develop, and they cannot be compressed onto a one-minute chart without dissolving into noise.

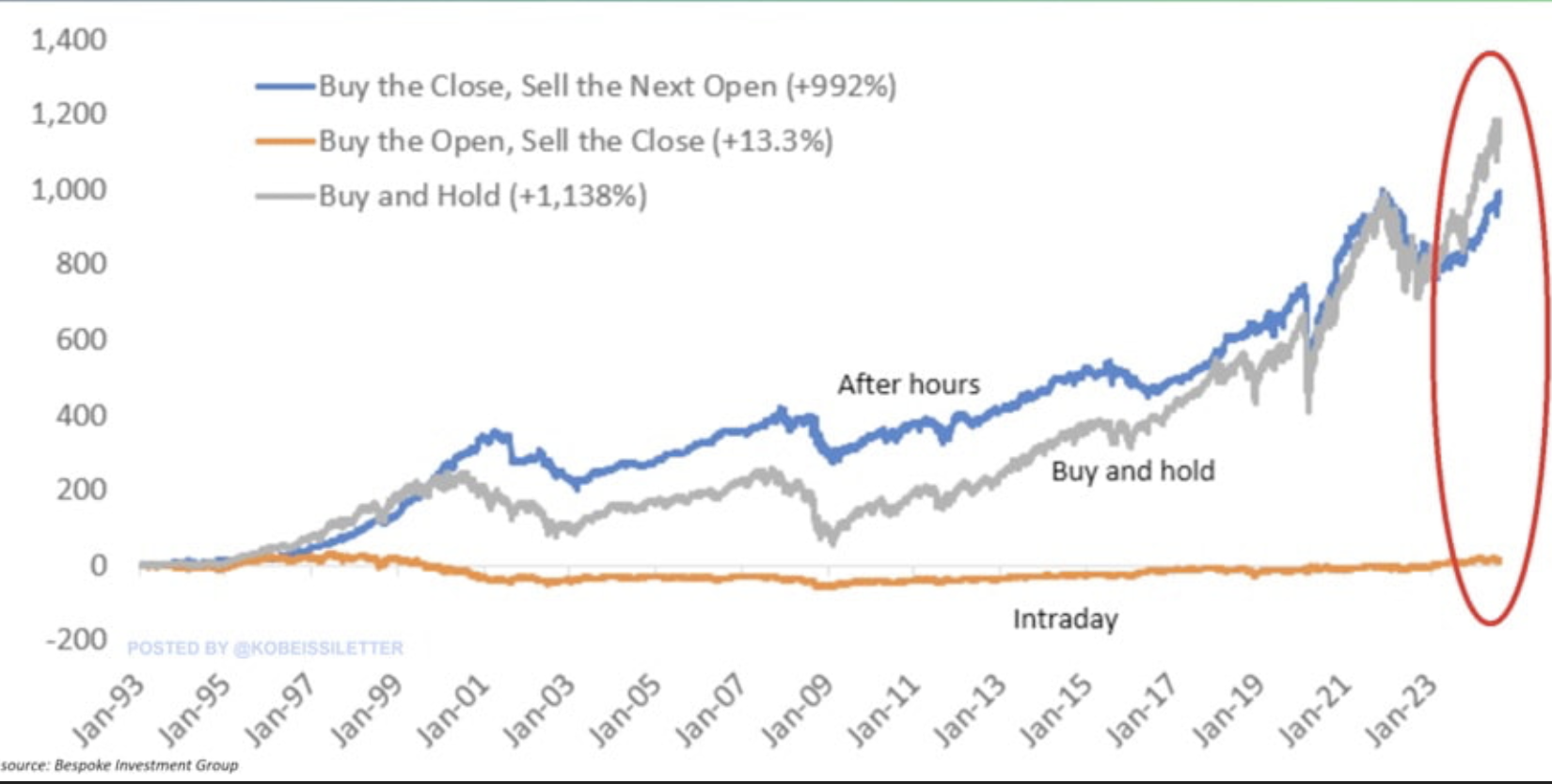

The market's own structure makes the case. Little decisive direction appears during the regular session. The larger share of movement occurs outside cash hours, where price frequently travels faster than the overall trend. A strategy that holds captures those periods; one that closes intraday does not.

Low-timeframe trading also carries three penalties at once. It exposes you to far more random, undirected price movement; it demands a considerably harder build, since an intraday mean-reversion system is far more complex than a momentum model on one-, three-, and six-month lookbacks; and it forces you to compete against high-frequency firms whose latency and infrastructure advantages retail can never match. A well-constructed factor model can return a similar annualised figure with a fraction of the technical difficulty, which is the entire point, since a method most traders can implement is worth more than a superior one only an engineer can run.

That is the foundation: swing account, factor models, medium-term horizon. The five rules follow from it.

Where to open a swing account

This guide runs on FTMO, but Alpha Capital Group and The5ers also offer swing accounts if you would rather use one of them. To get the discount, you must open the account through the link below and enter the code at checkout.

- FTMO — the swing account used throughout this guide.

- Alpha Capital Group — swing accounts available. Use code JULY4 for 30% off.

- The5ers — swing accounts available. Use code REYHG at checkout.

You must open the account through the link and enter the code at checkout for the discount to apply.

Rule 1: Follow the trend, and trade long only

Mean reversion is seductive on a backtest. It shows a high win rate and a large number of trades, which produces more winning weeks. In live conditions it decays quickly, typically within about five months, while trend-following systems endure. Several of mine have remained profitable for three years. Prop firm rules punish the difference severely, because one poor cluster of mean-reversion trades can breach the daily loss limit before the edge has any chance to recover.

The second half of the rule is to avoid shorts. Below the 200-day moving average, one of the most heavily studied regime filters available, volatility increases and the risk of a sharp reversal or an early stop-out rises with it. Beyond that, bear markets, where shorts would perform best, are historically far shorter than bull markets. The asymmetry rewards long, medium-term positioning.

Rule 2: Dollar-cost average into every position

Do not enter at full size. Begin at 10-20% of your intended position (the ceiling being the maximum risk level your Monte Carlo analysis identifies, per Rule 3), then add roughly 5% per week as the trend confirms.

The reasoning is structural rather than psychological. Trends need time to develop, and trend signals are least reliable at the very start, where a valid exit can appear before the move has matured. Scaling in gradually limits the loss when momentum fails to establish, allows a genuine trend to prove itself before full capital is committed, and increases exposure just as the trend gains velocity. It is, in effect, a hedge against the possibility that a position's first weeks are misleading.

Under a 5% daily loss limit, where a single oversized entry can end a challenge on a bad day, this discipline is not optional. Entering at full size is among the most common ways new traders fail evaluations, and correcting it is frequently the difference between passing and paying to retake the challenge.

Rule 3: Set allocation with a Monte Carlo simulation

There is no universal correct allocation. The right figure depends on your strategy, your drawdown profile, and your risk tolerance, and it should be derived from simulation rather than borrowed from a recommendation.

Take your strategy's return distribution, stop logic, and drawdown behaviour, and bootstrap thousands of equity paths across a range of allocation levels. Plotting pass rate against allocation produces a curve that generally peaks between 40% and 60%. Below that band, capital is deployed too slowly to reach the profit target within the time limit; above it, the account is too aggressive and risks a breach before the trend pays off. For most trend systems I have tested, the optimum sits near 50%, but the number only means something if it comes from your own data.

Once you have it, remain there. On any platform without a hard maximum-favourable-drawdown cap, time is the largest edge available, and patience operates as a form of position sizing.

Find your pass-rate optimum

Rule 3 in practice: run your win rate, risk and reward through the free Monte Carlo simulator and see your real odds across FTMO and 10 more firms.

Open the simulator →Rule 4: Calculate position size correctly

Failing to size positions accurately is the single most common cause of same-day liquidation, because most traders do not actually know how many lots they are buying.

The formula:

Lots = (Capital Allocated × Leverage) ÷ (Asset Price × Contract Size)

The complication is contract size, which differs by asset class: 1 unit per lot for equity CFDs, 100,000 for forex majors, 100 for gold and most metals and crypto CFDs, and platform-dependent values for indices. Leverage varies too: 30x on FTMO swing accounts, up to 100x on the more aggressive standard evaluations.

Worked example. For €25,000 of exposure to gold at roughly $5,015/oz on a 30x swing account with a contract size of 100: taken as unleveraged underlying exposure, this is about 0.05 lots; taken as €25,000 of margin deployed at 30x (a very different quantity), it is closer to 1.5 lots of notional. These two are routinely confused, so be certain which you intend.

Never rely on mental arithmetic here. The underlying difficulty is that MetaTrader does not ask how much money you want to risk; it asks how many lots, and because the lot convention was built for forex and later applied to everything else, a lot means something different for each asset. A single formula resolves it:

Lots = (Desired dollar exposure) ÷ (Price × Multiplier)

Only the multiplier changes.

| Asset | Multiplier | What 1.00 lot equals |

|---|---|---|

| Forex (any pair) | 100,000 | $100,000 of the base currency |

| Gold (XAUUSD) | 100 | $100 per $1 move |

| Silver (XAGUSD) | 5,000 | $5,000 per $1 move |

| Oil (USOIL, UKOIL) | 1,000 | $1,000 per $1 move |

| Indices (US30, US500, US100, GER40, UK100, JP225) | 10 | $10 per 1-point move |

| Crypto (BTC, ETH) | 1 | $1 per $1 move |

| Stocks (AAPL, TSLA, NVDA, etc.) | 1 | $1 per $1 move |

Verified for FTMO as of May 2026. Qualifications: oil may trade as a 100-barrel "mini" on some accounts; the JP225 multiplier changed from 5 to 10 in July 2025 (update older scripts); and altcoins beyond BTC, ETH, LTC, and DASH have variable contract sizes to check individually. The authoritative source is always the symbol specification in MT5 (right-click symbol, then Specification).

Prop firm documentation is consistently poor: contract sizes buried in dated PDFs, leverage terms in footnotes, FAQ pages that contradict the terms of service. Verify every figure against the platform's own specification rather than assuming.

Rule 5: Diversify to avoid a compliance ban

A profitable, consistent, fully rule-compliant account can still be closed for trading a single asset. This is not hypothetical: a trader I know passed an evaluation trading only gold, with genuine profit and clean execution, and was banned regardless, because the risk team classified single-asset concentration as gambling behaviour. Evaluation rules are less concerned with whether you are profitable than with whether you resemble a sustainable operation to a compliance officer.

The requirement is to hold positions across at least three asset categories: equities, forex, and metals, or forex, crypto, and indices. The specific combination is unimportant, only the spread. If your real conviction sits in one asset, a token 0.01-lot position in a low-volatility instrument satisfies the requirement at negligible cost.

Bonus: Weight allocations by volatility

Diversify intelligently by weighting inversely to volatility, so that an instrument capable of a 6% daily move does not carry the same weight as a stable one. A workable heuristic:

- High volatility (TSLA, NVDA, BTC): 3-5% each

- Medium volatility (AAPL, gold, EURUSD): 8-10% each

- Low volatility (BRK.B, AUDNZD): up to 15% each

This single adjustment is frequently what keeps an account inside the 5% daily loss limit on an adverse day, and the adverse day is what ends most challenges.

The asset shortlist

Trade only liquid, trending instruments, using five-year annualised CAGR as a first-pass filter, since a sustained long-term trend marks a viable candidate. FTMO's expanded equity universe puts the high-CAGR names (MSTR, NVDA, AVGO, PLTR, GOOG) where trends genuinely persist; GOOGL, AAPL, and Berkshire Hathaway also model well.

- Forex: the majors only, being EURUSD, GBPUSD, USDJPY, USDCHF, and USDCAD.

- Crypto: BTC and ETH only, sized conservatively.

- Metals: gold first (XAUUSD, XAUEUR), silver second, others only as token diversification.

Avoid exotic crypto pairs (DASH, DOT, BCH, ETC) and thinly traded metals such as palladium and platinum. Slippage on illiquid instruments erodes returns, and no risk manager will excuse an unusually wide spread.

Summary

- Trade an FTMO swing account; factor models are medium-term, so do not fight the timeframe.

- Follow trends and stay long: no mean reversion, no shorts.

- Dollar-cost average in at 10-20%, adding roughly 5% per week as the trend confirms.

- Allocate at the pass-rate optimum from your own Monte Carlo simulation.

- Calculate lots precisely and verify against the platform specification.

- Diversify across three or more categories, weighted inversely to volatility.

Time is the edge and patience is the position. The framework is not difficult; the failure is almost always in the execution of the simple parts.

Ready to put this into practice? You can open a swing account and start your challenge through FTMO here.

This post is for educational purposes only and does not constitute financial, investment, or trading advice. Trading carries a significant risk of loss, and past performance is no guarantee of future results. Do your own research and consider consulting a licensed professional before making any financial decision.

This post contains an affiliate link. If you sign up through it, I may earn a commission at no extra cost to you.

← Back to the simulator